CDs vs. Annuities: An Overview

Certificates of deposit (CDs) and annuities can each be good methods to avoid wasting for the longer term. Each kinds of funding supply a low-risk, low-return method of investing. Nonetheless, there are some vital variations between these monetary merchandise.

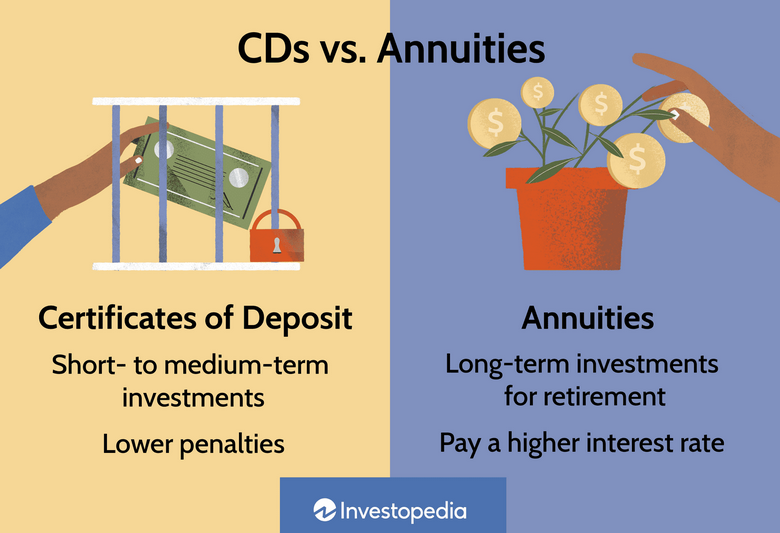

Crucial is the size of time that every sort of funding is designed for. Most individuals will use an annuity to avoid wasting for retirement—that’s, as a long-term funding. In distinction, CDs are greatest used for short- to medium-term investments. In case you are seeking to put apart some extra cash for retirement, an annuity could be a good possibility. In the event you’ll want that cash in 5 years, it’s higher to go for a CD.

- Each CDs and annuities are very protected investments. Each supply a set return in your cash and are insured or assured by the FDIC or insurers.

- CDs will be extra versatile than annuities, with shorter phrases and decrease penalties if it’s essential to withdraw your cash in an emergency.

- Annuities will usually pay a better rate of interest than CDs.

- Probably the most basic distinction between a CD and an annuity pertains to the period of time they’re designed to be held for—a CD is greatest for short- to medium-term investments and an annuity is normally a long-term funding for retirement.

Investopedia / Michela Buttignol

Certificates of Deposit

Threat

CD investments are protected by the identical insurance coverage that covers all deposit merchandise. The Federal Deposit Insurance coverage Company (FDIC) gives insurance coverage for financial institution prospects, and the Nationwide Credit score Union Administration (NCUA) gives insurance coverage for credit score union prospects. Whenever you open a CD with an FDIC- or NCUA-insured establishment, as much as $250,000 (per account, per account class) of your funds on deposit with that establishment are protected if that establishment have been to fail.

Liquidity

CDs are usually not probably the most liquid investments, however they’re extra liquid than annuities. It is because you're required to lock your funds into an account for a set interval. If it’s essential to get to those funds in an emergency, you'll be requested to pay penalties as a result of banks use the cash you give them (you're primarily loaning them cash in a CD). Withdrawing it early causes the financial institution to scramble for funds to exchange what you've withdrawn, so the penalties assist it make up a few of the losses induced.

Rates of interest

CD rates of interest are usually decrease than annuity charges however greater than these of financial savings accounts. This makes them a wonderful solution to protect your capital, particularly if their charges sustain or exceed the inflation fee. As a result of inflation chips away at worth, it's vital to make sure your CDs have a fee that can make them at the very least sustain with inflation—which financial savings account charges usually don't do.

Taxes

The curiosity you earn by a CD is taxed as abnormal earnings—it’s speculated to be reported as earnings in your annual tax submitting. CDs will be much less tax-efficient than annuities in some circumstances, however for most individuals, the opposite variations between these funding devices might be extra vital than the tax implications of every.

Be sure you perceive the early withdrawal penalties that apply to your annuity or CD account. If it’s essential to entry your cash in an emergency, you may pay hefty charges. These charges are usually greater for an annuity as a result of annuities are designed to be held for longer than a CD.

Annuities

Threat

Annuities aren’t insured by the FDIC or NCUA. Nonetheless, they’re usually insured by the issuing insurance coverage firm and, generally, by state warranty associations. Nonetheless, it’s vital to make sure your annuity is issued by a highly-rated insurance coverage firm to make this safety as robust as attainable.

Liquidity

Each CDs and annuities have early withdrawal penalties—that’s, each are pretty rigid funding automobiles since you should depart your cash in them for a specified time period. Nonetheless, as a result of annuities are usually designed to be held longer than CDs (till retirement, reasonably than only a few years), annuities can have greater penalties than CDs if it’s essential to get your a refund in an emergency.

Due to this, traders who’re contemplating buying an annuity ought to fastidiously contemplate their monetary necessities. Annuities normally have a give up interval, throughout which you can not make withdrawals with out paying a give up cost or charge. There are additionally tax implications for withdrawals from retirement annuities earlier than age 59½.

Rates of interest

Although annuities are much less versatile than CDs, this drawback is offset by a bonus—annuities usually pay a better rate of interest than CDs. It is because the monetary establishment you maintain your annuity with is uncovered to much less threat because of the longer size of time you’ll maintain it.

Relying on prevailing rates of interest, a distinction of simply 1% or 2% can have an effect on the long-term return in your investments. This could make an annuity an excellent possibility for older traders who’re unlikely to wish the liquidity provided by a CD and wish to preserve their investments low threat whereas incomes an affordable return.

Taxes

Annuities are designed for retirement and include tax benefits when used on this method. The curiosity your annuity earns is tax-deferred, so that you pay taxes solely once you start withdrawing from it. Withdrawals are taxed on the similar tax fee as your abnormal earnings. In the event you fund an annuity by a person retirement account (IRA) or one other tax-advantaged retirement plan, you may additionally be entitled to a tax deduction on your contribution. This is called a certified annuity.

Particular Concerns

There are a number of kinds of annuities, however they’re primarily used for retirement functions—to assist people deal with the chance of outliving their financial savings. An annuity usually pays you an earnings stream over time. This makes an annuity appropriate for folks seeking to safe a gentle earnings stream in retirement.

CDs include totally different maturities and pay you a lump sum after they mature. So, CDs are extra suited to these wanting to save cash for a short-term aim. Nonetheless, you need to use CDs to design earnings streams utilizing a CD ladder method. Fairly than rolling them into one other CD, you need to use the proceeds as earnings as they mature and payout.

Is an Annuity Higher Than a CD?

It relies upon. If you wish to save within the brief time period, a CD can supply extra flexibility than an annuity. An annuity is a more sensible choice if you wish to guarantee a gentle earnings stream in retirement.

Are CDs and Annuities Protected?

Sure. Each kinds of funding are insured—CDs by the FDIC or NCUA and annuities by the issuing insurance coverage firm. Generally, state warranty associations additionally add safety. It’s vital to decide on a monetary establishment you belief, however your cash must be protected in both sort of funding.

What Are Early Withdrawal Penalties?

Each CDs and annuities have charges and penalties should you withdraw your cash early. You must depart your cash within the CD for the time period you’ve agreed to, otherwise you’ll most likely need to pay sizable early withdrawal penalties that might wipe out your returns. Equally, annuities have a give up interval, throughout which withdrawals will incur a deferred gross sales charge. This era usually spans a number of years.

The Backside Line

Each CDs and annuities are very protected investments. Each supply a set return in your cash and are assured or insured.

There are variations, nevertheless. CDs will be extra versatile than annuities, with shorter phrases and decrease penalties if it’s essential to withdraw your cash in an emergency. Annuities will usually pay a better rate of interest than CDs. A CD is greatest for short- to medium-term investments and an annuity is best for a long-term funding in your retirement.